By: ROBIN JASPERT

The utmost part of equity of GSE-listed companies is held by foreign institutional investors. If the Ghanaian economy is to strive and serve its people, this must change.

The profits reaped out of Africa flow into the hands of foreign capitalists. This is because foreign financial capital owns the continent’s companies – and these own the means of production.

Everyone who engages with Africa’s political economy knows that profit made on the continent tends to flow abroad. The fruits of the continent’s labour are harvested elsewhere – and mostly in the North. This held true in times of colonialism as it does under the current conditions of capitalism and neocolonialism. Such has been pointed out, among others, by Kwame Nkrumah who meticulously analysed ownership structures of some of the continent’s biggest corporates. Writing in the 1960s, Nkrumah unpacked the structure of Anglo-American Corporation. He analysed in detail how The British South Africa Company and Rio Tinto were organised. In Neo-Colonialism: The Last Stage of Imperialism, Nkrumah dedicates almost half of his analysis to corporate structures.

He was right to do so. Private companies own a major share of the means of production in any capitalist economy. Even more importantly, stock companies are the ones holding the means of production in the economic sectors which are most profitable. Ever since the joint stock company was developed to foster the colonial plunder of Asia and India in particular, it has become the dominant legal form for multinational private companies. Historically, these were key drivers of the colonisation, plunder and exploitation of the South. And today?

Today’s Grip

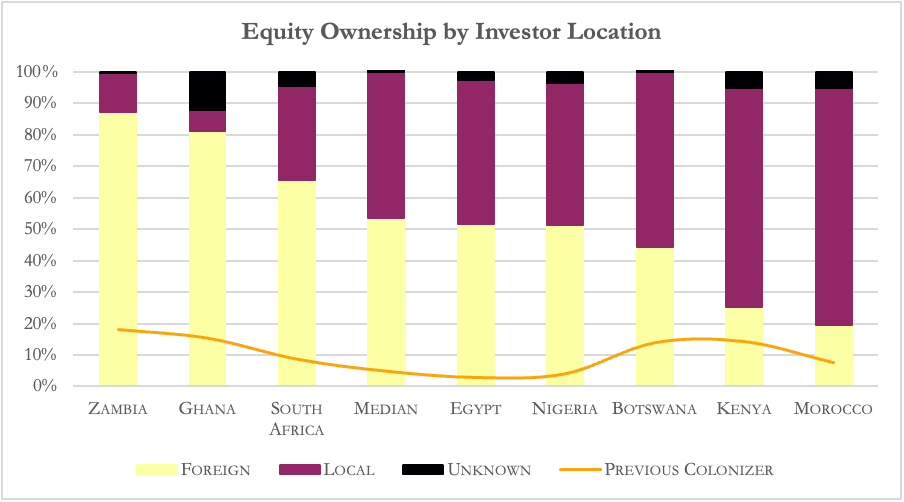

To bring our analyses up to speed, in this article I take a look into the contemporary ownership structures of African-based corporates. It helps to understand today’s mechanisms of neocolonial plunder. With this purpose, I created a dataset with Bloomberg Terminal data[i] on the eight biggest equity markets on the continent with solid data availability.[ii] These are Botswana, Egypt, Ghana, Kenya, Morocco, Nigeria, South Africa and Zambia. In these countries, on average, 54% of corporate ownership in stock listed companies of the biggest stock market is held by foreign investors.

Sit with this for a minute. More than half of the ownership of the continent’s stock-listed companies in these key economies is held abroad. For Zambia, this number reaches a staggering 87%. On weighted average, 11% of the shares are held by financial actors in the former colonising power – which for most of the countries in this dataset is the United Kingdom. The United States are big in the game, too. In South Africa they hold more than 30% of the equity. And not to forget the tax havens.

In Ghana, the dubious Investcom Consortium Holdings based on the British Virgin Islands holds 77% of Scancom, better known as MTN Ghana. MTN Ghana is with some distance the heavyweight of the Ghanaian Stock Index GSE. Forced by a due diligence process, Investcom Consortium Holdings sold a small share of their holdings to the Ghanaian directors of the company at the end of 2024 – exactly because the issue has such heavy political significance. In Nigeria the single biggest investor of the NGX stock index is MTN International Mauritius. With about 74% they are the biggest shareholder of MTN Nigeria and channel their money into the tax haven Mauritius.

Source: Author creation based on Bloomberg Terminal data

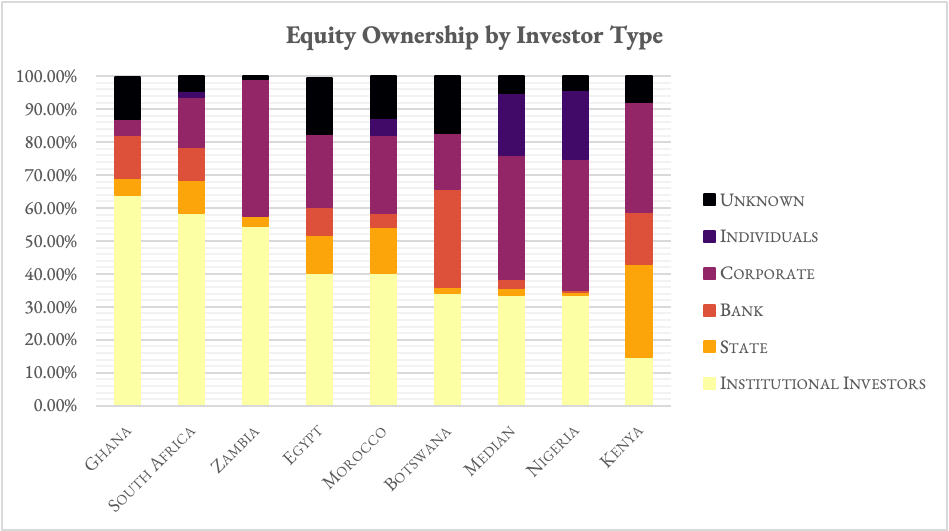

Another revealing insight arises when analysing the ownership structures by investor type. But for some exceptions, the dominant players are institutional investors. This category includes asset managers, private-equity, hedge funds, holding companies and investment advisors. One does not err to name them financial capital. And so, financial capital holds more than 60% of stock listed companies in the main Ghanaian equity index.

On top of this, the average share of corporate ownership is high across all eight countries. And guess what: a large part of this is multinational companies who have their subsidiaries on the continent or bought up formerly local run businesses and incorporated them. In Kenya, Vodafone Kenya is the majority shareholder of Safaricom, owning almost 40% of the company and recently having agreed to increase their holding to 55%. By market capitalisation, Safaricom is by far the largest player in the NSE, the key Kenyan stock index. Their profits flow abroad after the local management extracted their share.

In Ghana, GSE-listed stock companies paid a total of 10.64 billion Cedi of dividends in 2024. Taking the end of year exchange rate this amounts to roughly 724.2 million USD. As 81% of shares are foreign held, 586,6 million USD go abroad. This does not include the profits investors make through gains in equity value. The GSE climbed about 75% in 2025. The total foreign investment in the index stands at a minimum of 93 billion USD. Excluding exchange rate and inflation developments for simplicity, this amounts to a rise in stock value of roughly 40 billion USD. This is only one year in one of the eight respective countries. And the African continent totals 55.

Whose Means?

These structures systematically transfer value created in the African economies abroad and mostly to the global North. While the details significantly differ across these eight states and are sure to be even more diverse across the 55 states on the continent, the overall picture is clear: foreign financial capital plunders the African continent through stock companies. Might it be any better for African workers to be exploited by local capital? If we follow the Brazilian economist Mauro Marini in his understanding of super-exploitation, no. Under conditions of dependent accumulation, local capitalists are forced to pay below subsistence wages to maintain competitiveness as much as foreign capitalists. Yet it is clear that if these massive profits did not flow abroad, African economies and governments would be far better positioned to face the drastic capitalist crises of our time – even though, ultimately, the working class on the continent would fare best if the means of production were in their hands.

[i] Data was gathered in August 2025, except for the South African case where data is from August 2024. Stock indices that were taken as baseline are the BGS, EGX, GSE, JALSH, LuSE, MASI, NGX and NSE. Not all investor information is being publicly disclosed, of course. Nonetheless, the overall coverage levels of the dataset are high enough for the data to give a reliable picture of the situation. There is no better information available than Bloomberg data. And based on prior experience of working with Bloomberg data there is no reason to assume the missing data would create a bias.

[ii] The methodology has been developed in a joint research endeavour with my much-valued colleague Johannes Petry.

Robin Jaspert is a PhD-researcher and political economist at the Goethe University in Frankfurt / Germany. His work focuses on the political economy of financial markets, north-south-relationship, fiscal and monetary policy. He approaches these topics adopting a critical economy perspective and a mix of quantitative and qualitative methods. Next to his scholarship, he is active as a freelance writer and journalist and facilitates educational seminars for the union.